Dec 12

preview

For a primer on what are interest rates, what moves them and how to trade them, please refer to our Interest Rates Primer.

Why are rates at their historic lows: After the Great Financial Crisis of 2008 monetary policy makers decided to lower interest rates to help the economy recover. They did so by cutting the benchmark rate that sets daily interest rates, as well as buying government bonds to curtail the longer-term cost of borrowing.

How does that impact global markets: Reducing the return investors can get from risk-free assets pushes them to buy riskier assets - from safe AAA bonds to riskier equities. Monetary easing props the entire global market.

Can rates keep falling: Yes they can, just look at Japan. A combination of slower growth and demographics might cause persistent low inflation and anchor rates where they are.

What if rates rise again: Then savers will be happy because they will gain more interest on their savings. At the same time, it is likely that the bull market in equities takes a breather as investors flow back into bonds.

Interest rates across Developed Markets are at or close to their all-time lows.

This is a legacy of monetary policy innovations and directives embraced since the Great Financial Crisis of 2008 - but it continues a long-term trend that started at the beginning of the 80’s.

In the latest decade, monetary policy authorities have used interest rate cuts and liquidity injections to ease the financial crisis (‘08), support European bond markets during their sovereign credit crisis (‘10) and most recently to spur markets during the Coronavirus crisis (‘20). In the background of this, Japan has continued its decades-long QE experiment and also Emerging Markets have injected liquidity in their markets.

The channel through which banks control rates is fairly simple:

The result is to push yields low so that everybody in the economy benefits from a low-rate environment. This approach when pushed to the extreme consequences can push interest rates into negative territory, with effects that are debated among economists.

On the longer horizon, if you look at the chart above you can see that rates have been on a downward trend for a long while. This has been driven by a large set of factors impacting inflation globally

The first hit to inflation was the Volker-engineered recession of 1980-1982, which drove inflation down from double-digit to close to 0% by the mid-80’s

This effect was compounded by three large factors:

The injection of liquidity and the direct lowering of rates achieve the same effect - they make bonds yield less and in some cases much less.

This has a very strong effect on the decisions of all investors, pushing capital “up the risk curve”: effectively, when an investor is deprived of buying a safe treasury bond at an acceptable rate, she is then forced to seek the same returns in riskier strategies.

This phenomenon is clearest in pension funds: pension schemes have clearly defined return targets in order to serve all their contributors, but they also have clear risk requirements that do not allow them to go into risky asset classes indiscriminately.

So a pension fund seeking an 8% long-term return and faced with Treasuries at 2% yield or less is forced to look at riskier assets. Maybe it can capture a 3% return from AAA bonds but again, that is not enough. It can allocate maybe 40% of its portfolio to equities on the assumptions that they can return 8%+ over the long term, but again that is not enough. Soon the fund is pushed into the riskiest asset classes - junk bonds and alternative investments.

If pension funds move heavily into equities and other risky asset classes, they naturally propel the prices higher, and provide fuel for the same kind of allocations by other investors that seek to achieve higher returns.

Are we in a bubble?

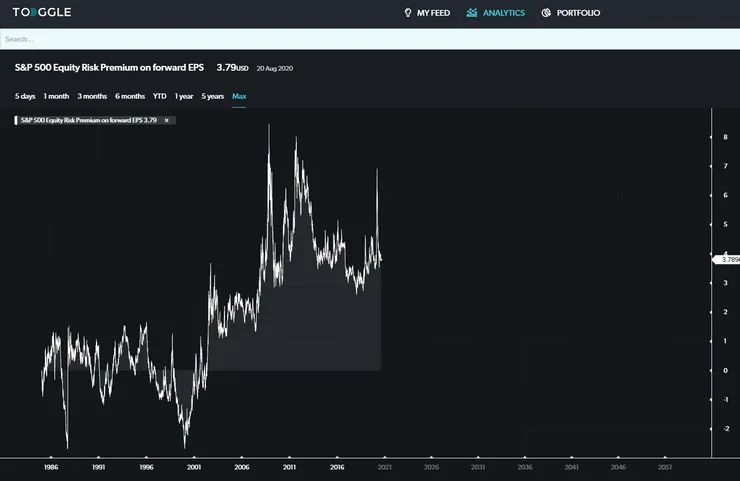

Looking at equity prices one would see the clear making of a market bubble. The reality is that equities are very cheap compared to bonds. The chart below shows the spread between the yield of equities and that of bonds: high means equities are cheap, low means bonds are cheap.

What we are experiencing is effectively a bond market bubble - which is exactly the same as saying “interest rates are a their all-time lows”

Yes they definitely can. Japan is the most commonly used example of this scenario - an ageing country with an unending QE program that has experienced a multi-decade long spell of close-to-nil inflation.

Rates in Japan have kept falling for a long time, finally finding (and piecing) the 0 bound in 2016. Japanese Government Bonds (JGBs) have been a permanent target of fundamental investors who considered them overpriced and unsustainably levered - only to be proven wrong again and again. The bonds have notoriously earned the nickname of widowmakers.

There is of course another scenario where rates finally start rising again, with causes that can be more or less benign.

In the positive scenario, the world’s economy recovers a healthy pace of inflation led by stronger wages and this in turn pushes the central banks to unwind their balance sheets (e.g. suck liquidity back in) and to hike rates. This scenario would see bonds fall in price but yields rise allowing savers to achieve better returns.

In the opposite direction, the massive injection of liquidity in the system might lead to run-away inflation, which would force central banks to hike much more aggressively - resulting in all likelihood in a recession that also leads to a pop in bubbly market valuations.

Investing in a Low-interest Rate World

Up Next

Dec 12

preview