Dec 12

preview

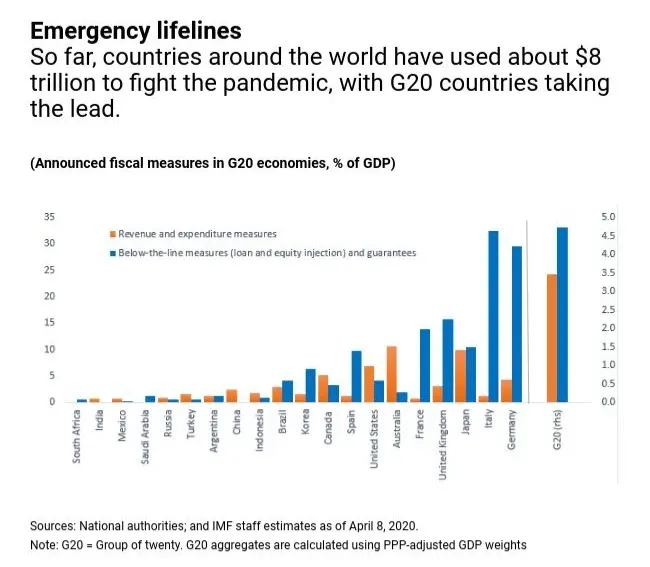

Trying to divine market outcomes in today’s environment feels similar to putting on a pair of bifocal glasses: looking up vs down, your perspective on the issue will either be crystal clear or totally muddled. Take the economic lens: we have seen unprecedented speed and magnitude of policy action, both fiscal and monetary, breaking many taboos along the way. Few would have expected the Fed, who in 2009 hemmed and hawed before buying US Treasuries, to dive headfirst into the junk bond market. Similarly, having a Republican president work with the US congress in a display of pandemic socialism, speedily approving a mammoth fiscal stimulus package that’s sending checks directly to the American public. These types of unprecedented moves have been mirrored around the world. Startlingly, Germany stands with Italy on top of the pile as the most aggressive spenders.

Only months into the COVID crisis, total fiscal spending by governments around the world has already far surpassed the total from the Great Recession, and many more packages are planned.

In a run-of-the-mill economic crisis, such swift action would likely be rewarded by rapid recovery in risky asset prices as investors perceive tail risks to have been successfully cut off.

Buy EVERYTHING. Switching to the public health lens, things become murkier. With so much uncertainty surrounding basic facts about COVID-19, the likelihood of speedy resumption of economic activity seems distant. What is the mortality rate? How many people are infected? Can you be reinfected, having survived it once, and how soon after? Even if government lockdown orders are lifted gradually, few are likely to head straight for the airports and railway stations. Patrons will be reluctant to frequent restaurants for fear of sitting next to strangers that could unknowingly be carrying the virus. Without a vaccine, a drug, or proper testing infrastructure, economic life could be severely limited for a long time to come. Stimulus checks and forgivable loans might therefore go to businesses that could have survived a short lockdown but are unlikely to make it through a full year of curtailed activity. A longer recession could easily turn into a full-blown financial crisis. Levered corporates may be unable to make payments. Banks, considered well-capitalized for even a 10% stress-test drop in GDP, will find themselves short on capital in a 20-30% one. Sell EVERYTHING. As the global economy and global pandemic crash into each other, predicting possible outcomes and interaction between these two complex dynamic systems becomes extremely difficult. Epidemiologists and Economists struggle to model these systems, even in absence of the added complexity of mutual interdependence. As a result, making a medium term (3-6 month) call on the market seems almost impossible. This is where the less path-dependent, longer-horizon investors have a massive advantage. The issue with both the Coronavirus and the economic recession isn’t that we don’t know how to address them, it’s that we don’t know how to address them fast enough to prevent lasting damage. But address them we will. In fact, it’s very likely a vaccine or a drug will be widely available by the middle of 2021. A possible portfolio approach today therefore begins by working backwards from the future: what do we think the world will look like in 2022? What companies and businesses will thrive among those we are able to invest in today?

Investing During a Pandemic

Up Next

Dec 12

preview